What decentralized KYC actually does

Decentralized KYC vaults function as privacy-preserving storage layers that sit between you and the verifier. Instead of sending raw personal identification information to a centralized company database, your data stays in a user-controlled vault. This shift moves ownership from institutions to individuals, ensuring that sensitive documents are never stored in a single, vulnerable repository.

This architecture eliminates the need to duplicate onboarding efforts across multiple platforms. As noted by Intellect Eu, the system enables institutions to sync data and documents, guaranteeing a single, golden copy of each client. Whenever a client is onboarded or their data is updated at any institution within the network, that update propagates securely. This keeps data current while eradicating duplicates and reducing the administrative burden on both the user and the compliance team.

The underlying infrastructure pairs AI verification agents with a substrate that shifts personal data from company databases into user-owned vaults. By eliminating PII from the verifier's direct access, the system reduces liability and enhances privacy. You verify your identity once, and the vault provides cryptographic proof to any institution that needs it, without exposing the raw underlying documents.

Market Landscape and Key Providers

The decentralized KYC vaults market is moving from experimental pilots to operational infrastructure. The shift is driven by the need to eliminate redundant verification cycles while maintaining regulatory compliance. Instead of storing personally identifiable information (PII) in centralized databases, these solutions place credentials in user-owned vaults. This architecture reduces liability for institutions and gives individuals control over their data sharing.

Current providers fall into two main categories: those offering substrate-based vaults and those focusing on network-wide synchronization. Zyphe, for example, pairs AI verification agents with a substrate that shifts personal data from company databases into user-owned vaults, effectively eliminating PII storage risks for the verifier. On the other side, Intellect's Catalyst Blockchain Manager focuses on syncing data and documents across a network to guarantee a single, golden copy of each client. This ensures data remains up-to-date and eradicating duplicates as clients move between institutions.

Entrust approaches the problem through a decentralized identity model designed specifically for banks. Their solution aims to solve existing challenges of sharing KYC information securely and cost-effectively. By treating identity as a decentralized asset rather than a stored record, these platforms are redefining how financial institutions handle onboarding and ongoing compliance.

Provider Comparison

The following table compares the core approaches of leading infrastructure providers in the decentralized KYC space.

| Provider | Core Mechanism | Data Ownership | Target Market |

|---|---|---|---|

| Zyphe | AI verification + User vaults | User | General enterprise |

| Intellect Catalyst | Blockchain synchronization | Network/Collaborative | Banking & Finance |

| Entrust | Decentralized Identity Model | User/Institution | Banks & Regulated Entities |

The transition from legacy KYC to these decentralized systems is not just technical but economic. By reducing the cost of verification and data storage, institutions can reallocate resources toward more complex compliance tasks. As the market matures, we expect to see more specialized providers emerging to address niche regulatory requirements across different jurisdictions.

How the vault stores and verifies data

A decentralized KYC vault operates as a privacy-preserving buffer between the user and the verifier. Instead of transmitting raw personally identifiable information (PII) like passport scans or home addresses, the vault holds the encrypted documents and manages the cryptographic proofs required for compliance. This architecture ensures that institutions can verify a client’s status without ever seeing the underlying sensitive data.

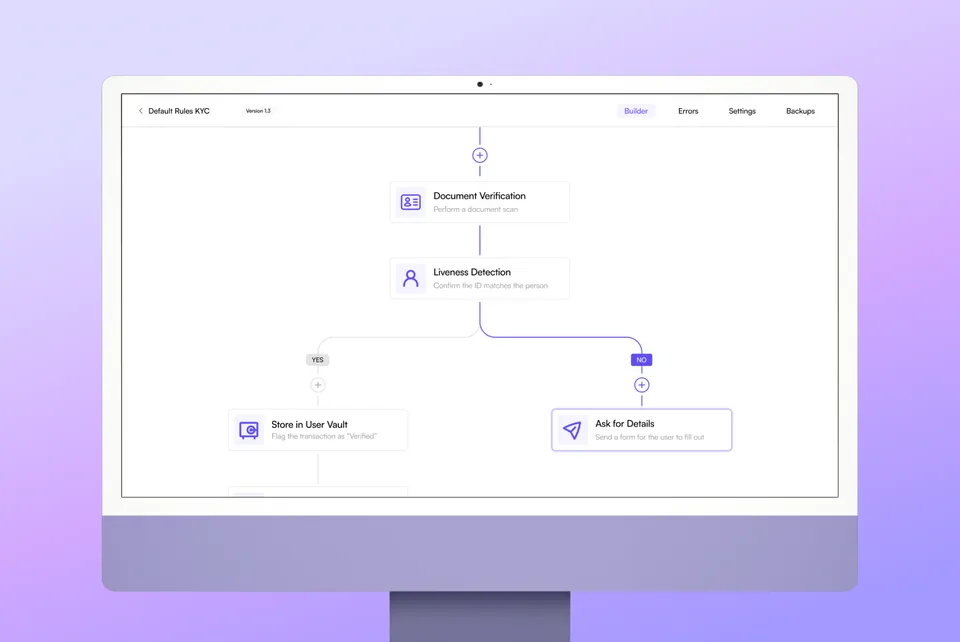

The workflow begins with Decentralized Identifiers (DIDs). When a user registers, they generate a DID—a unique, blockchain-resolvable identifier that they control. This identifier acts as the user’s digital persona, decoupling their identity from centralized databases. The DID serves as the anchor for all subsequent interactions, allowing the user to prove they are who they claim to be without revealing their central identity registry.

Next comes credential issuance. Once the user’s identity is verified by a trusted issuer (such as a government body or a licensed bank), a Verifiable Credential (VC) is issued. This credential is cryptographically signed by the issuer and stored in the user’s vault. It contains specific claims—such as "over 18" or "citizen of Germany"—but remains encrypted until the user decides to share it. The vault essentially becomes a secure, personal ledger of these trusted attestations.

The final step is zero-knowledge proof (ZKP) verification. When a service provider needs to onboard the user, they request a proof rather than the data itself. The vault generates a ZKP, which mathematically demonstrates that the user meets the criteria (e.g., age > 18) without revealing the actual birth date. This allows for instant, private compliance checks. The verifier accepts the proof, and the transaction is complete, leaving no raw PII exposed on the network.

The user creates a DID on a supported blockchain or distributed ledger. This unique identifier becomes their permanent, user-controlled identity anchor, replacing traditional centralized account logins.

After initial verification by a trusted issuer, the user receives signed credentials. These are encrypted and stored locally in the decentralized KYC vault, ensuring the user retains sole custody of their data.

When a verifier requests specific data, the vault generates a cryptographic proof. This proof confirms that the user meets certain criteria (e.g., age, residency) without exposing the underlying personal information.

The verifier checks the ZKP against the issuer’s public key. If valid, access is granted instantly. The entire process leaves no raw PII on the blockchain, maintaining strict privacy and regulatory compliance.

To understand the broader market context of this infrastructure, it is helpful to look at the underlying asset dynamics driving adoption. The volatility and trading volume of major cryptocurrencies often correlate with institutional interest in decentralized identity solutions.

Compliance strategies for regulated markets

Navigating the intersection of decentralized identity and strict regulatory frameworks requires a shift from data hoarding to data verification. In traditional models, institutions store vast amounts of sensitive personal information, creating high-value targets for breaches. Decentralized KYC Vaults change this dynamic by allowing users to hold their own credentials while proving compliance to regulators on demand. This approach aligns with the principle of data minimization, ensuring that only the necessary information is shared for each specific interaction.

For regulated markets, the primary challenge is balancing privacy with the requirements of Anti-Money Laundering (AML) and Know Your Customer (KYC) laws. Decentralized systems meet these obligations by using cryptographic proofs rather than raw data transfer. When a user interacts with a platform, they can generate a zero-knowledge proof that confirms they are over 18, are not on a sanctions list, or reside in a permitted jurisdiction, without revealing their actual birthdate or address. This preserves the "golden copy" of the client's data at the source, preventing the proliferation of duplicate or outdated records across the network.

Regulators are increasingly recognizing the value of this infrastructure. By adopting decentralized KYC vaults, financial institutions can reduce the friction of onboarding while maintaining a robust audit trail. The focus shifts from verifying identity through document submission to verifying the validity of a cryptographic credential issued by a trusted authority. This not only enhances security but also streamlines the compliance process, making it more scalable for high-volume digital asset platforms.

The credibility of this infrastructure is tied to the stability and adoption of the underlying digital assets. As decentralized finance (DeFi) and tokenized assets mature, the need for compliant on-ramps and off-ramps becomes critical. Market volatility does not diminish the legal necessity of identity verification; rather, it highlights the need for resilient compliance layers that can operate independently of price fluctuations.

Ultimately, successful implementation requires a partnership between technology providers and legal teams. The goal is to create a system where compliance is not a bottleneck but a built-in feature of the user experience. By leveraging decentralized KYC vaults, regulated markets can offer the privacy and security that users expect while satisfying the rigorous demands of global financial authorities.

How to integrate decentralized KYC workflows

Integrating decentralized KYC vaults requires shifting from centralized data hoarding to a privacy-preserving sync model. Instead of institutions storing raw user documents, vaults act as intermediaries that verify identity while keeping the golden copy of the client’s data synchronized across the network. This approach ensures that whenever a client is onboarded or updated at one institution, the change propagates securely to all authorized participants, eliminating duplicates and reducing compliance overhead.

To implement this infrastructure, start by selecting a compliant Decentralized Identifier (DID) framework that supports zero-knowledge proofs. Verify that your chosen verification agents can interact with the vault without exposing sensitive raw data. This selection phase is critical for maintaining regulatory alignment while leveraging the efficiency of decentralized ledgers.

Once the framework is chosen, focus on the integration of verification agents. These agents handle the cryptographic handshake between the user, the vault, and the verifier. Ensure your technical team tests the data sync protocols thoroughly to guarantee that updates are reflected in real-time across all network nodes. This step transforms static KYC records into dynamic, self-sovereign identity assets.

Checklist for implementation:

-

Audit current KYC data silos and map integration points

-

Select a DID framework with regulatory approval in your jurisdiction

-

Configure verification agents for zero-knowledge proof generation

-

Test end-to-end data synchronization with a pilot user group

-

Establish ongoing compliance monitoring for vault updates

Common questions about decentralized identity

Decentralized KYC (DID) shifts the burden of identity verification from individual institutions to a shared, trusted network. Instead of submitting documents repeatedly to every bank or exchange, a user verifies their identity once and shares a cryptographic proof with any institution in the network.

This approach creates a "golden copy" of client data that is updated in real time. When a client’s information changes at one institution, the update syncs across the entire network, ensuring all parties have the most current, accurate data without redundant processing.

What is decentralized KYC?

Decentralized KYC enables institutions to sync data and documents, guaranteeing a single, golden copy of each client and associated natural persons. Whenever a client is onboarded or their data is updated at any institution within the network, this ensures data is kept up-to-date while eradicating duplicates. The system relies on distributed ledger technology to maintain integrity without a central authority.

How does it differ from traditional KYC?

Traditional KYC stores data in silos, requiring users to re-verify for every new service. Decentralized KYC uses self-sovereign identity principles, allowing users to control their data. Institutions receive only the necessary verified attributes (e.g., "over 18," "passed AML check") rather than raw documents, reducing privacy risks and compliance overhead.

Is decentralized KYC compliant with regulations?

Yes, when implemented correctly. Solutions like the Intellect Catalyst Blockchain Manager align with global standards by providing an immutable audit trail. Regulators can verify the source of truth without accessing sensitive personal data directly, satisfying GDPR and AML requirements through privacy-preserving cryptography.

No comments yet. Be the first to share your thoughts!